EDMS 657-R Tutorial: Tree-based Methods

Yi Feng

EDMS, University of MarylandFirst, let’s load all the required packages.

install.packages("tree")

install.packages("randomForest")

install.packages("rpart")

install.packages("caret")

install.packages("rpart.plot")

install.packages("gbm")

library(tree)

library(randomForest)

library(rpart)

library(caret)

library(rpart.plot)

library(gbm)

library(EDMS657Data)Regression Trees

We will use the Major League Baseball Data for the demonstration of regression trees. In this example, we are interested in predicting the log-transformed salary.

We first fit the regression tree to a subset of the baseball data, predicting the log transformed salary.

data("hitters")

# log transform the salary

hitters$lgSalary <- log(hitters$Salary)

# you can use the tree package

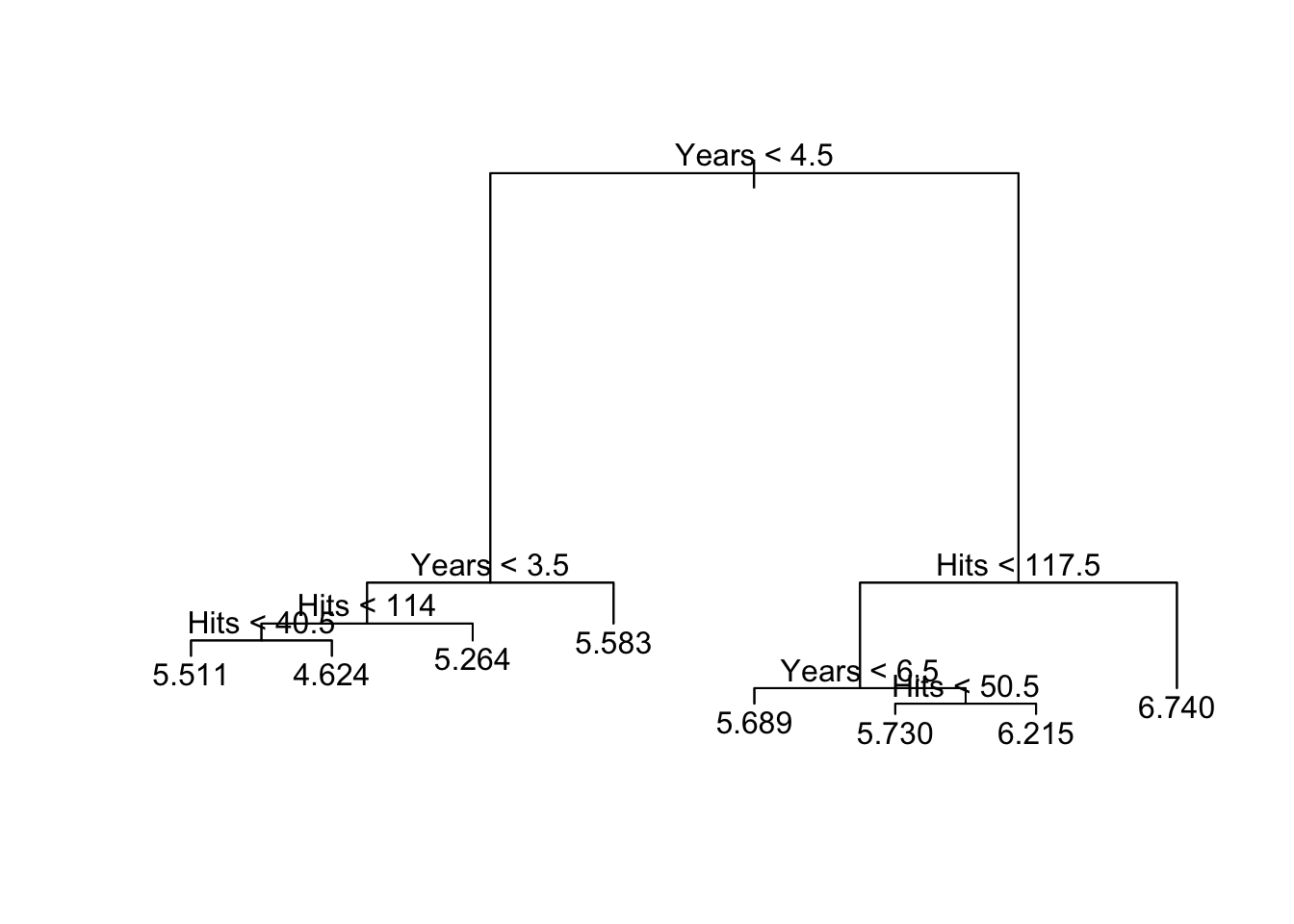

tree.hitters <- tree(lgSalary ~., hitters[is.na(hitters$Salary) == F, c("lgSalary","Years","Hits")])

summary(tree.hitters)##

## Regression tree:

## tree(formula = lgSalary ~ ., data = hitters[is.na(hitters$Salary) ==

## F, c("lgSalary", "Years", "Hits")])

## Number of terminal nodes: 8

## Residual mean deviance: 0.2708 = 69.06 / 255

## Distribution of residuals:

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## -2.2400 -0.2980 -0.0365 0.0000 0.3233 2.1520# you can also use the rpart package

tree.hitters_2 <- rpart(formula = lgSalary ~.,

data = hitters[is.na(hitters$Salary) == F, c("lgSalary","Years","Hits")],

method = "anova",

control = list(cp = 0.005))

tree.hitters_2## n= 263

##

## node), split, n, deviance, yval

## * denotes terminal node

##

## 1) root 263 207.153700 5.927222

## 2) Years< 4.5 90 42.353170 5.106790

## 4) Years< 3.5 62 23.008670 4.891812

## 8) Hits< 114 43 17.145680 4.727386

## 16) Hits>=42 36 3.098678 4.637745 *

## 17) Hits< 42 7 12.269990 5.188399 *

## 9) Hits>=114 19 2.069451 5.263932 *

## 5) Years>=3.5 28 10.134390 5.582812

## 10) Hits< 106 14 1.791944 5.315652 *

## 11) Hits>=106 14 6.343952 5.849973 *

## 3) Years>=4.5 173 72.705310 6.354036

## 6) Hits< 117.5 90 28.093710 5.998380

## 12) Years< 6.5 26 7.237690 5.688925 *

## 13) Years>=6.5 64 17.354710 6.124096

## 26) Hits< 50.5 12 2.689439 5.730017 *

## 27) Hits>=50.5 52 12.371640 6.215037 *

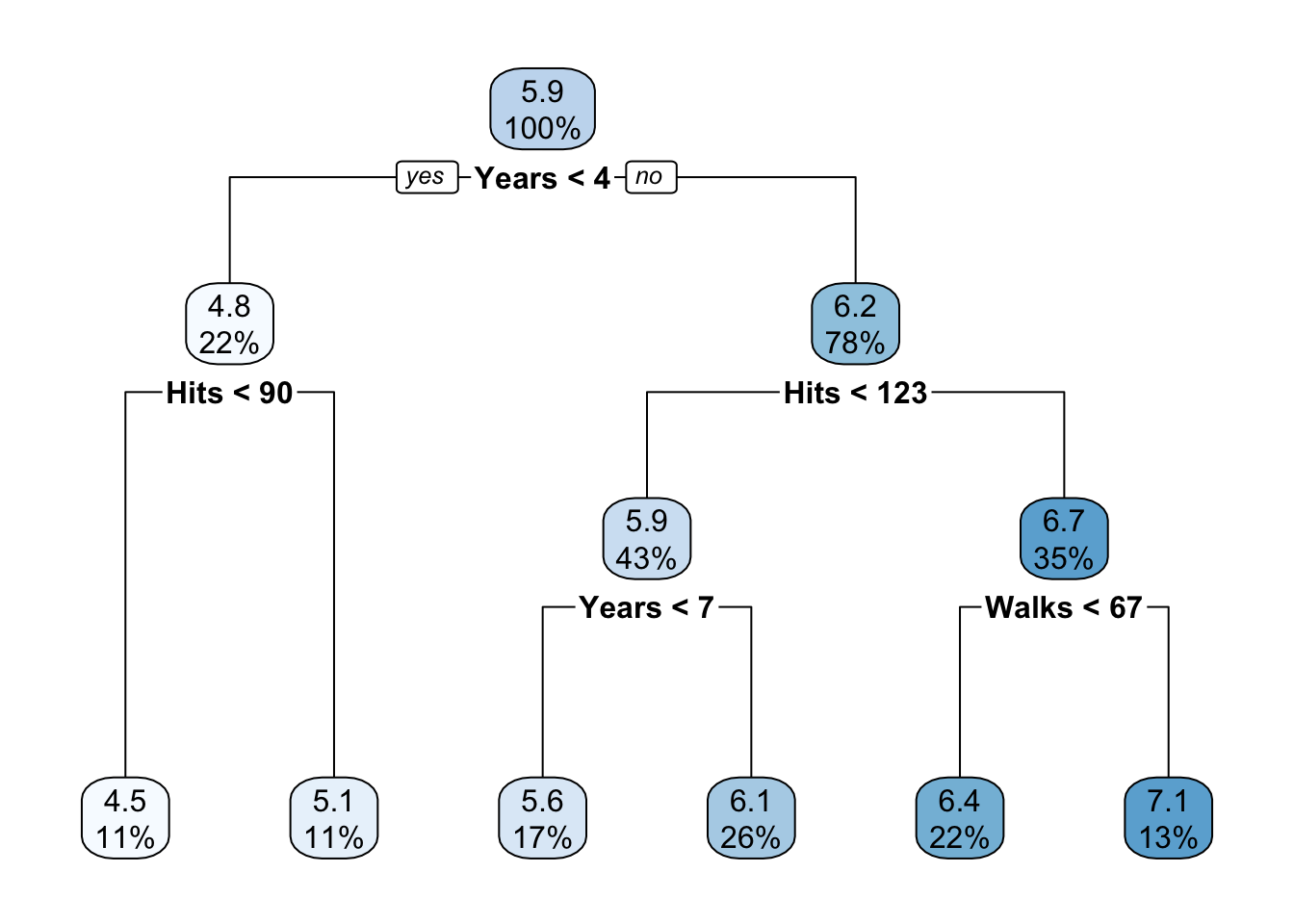

## 7) Hits>=117.5 83 20.883070 6.739687 *we can plot the regression tree.

# if you are using the tree package

plot(tree.hitters)

text(tree.hitters, pretty = 0)

# if you are using the rpart package

rpart.plot(tree.hitters_2)

To avoid over-fitting, we should consider pruning the tree. Here we try to only keep 3 terminal nodes.

# if using the tree package

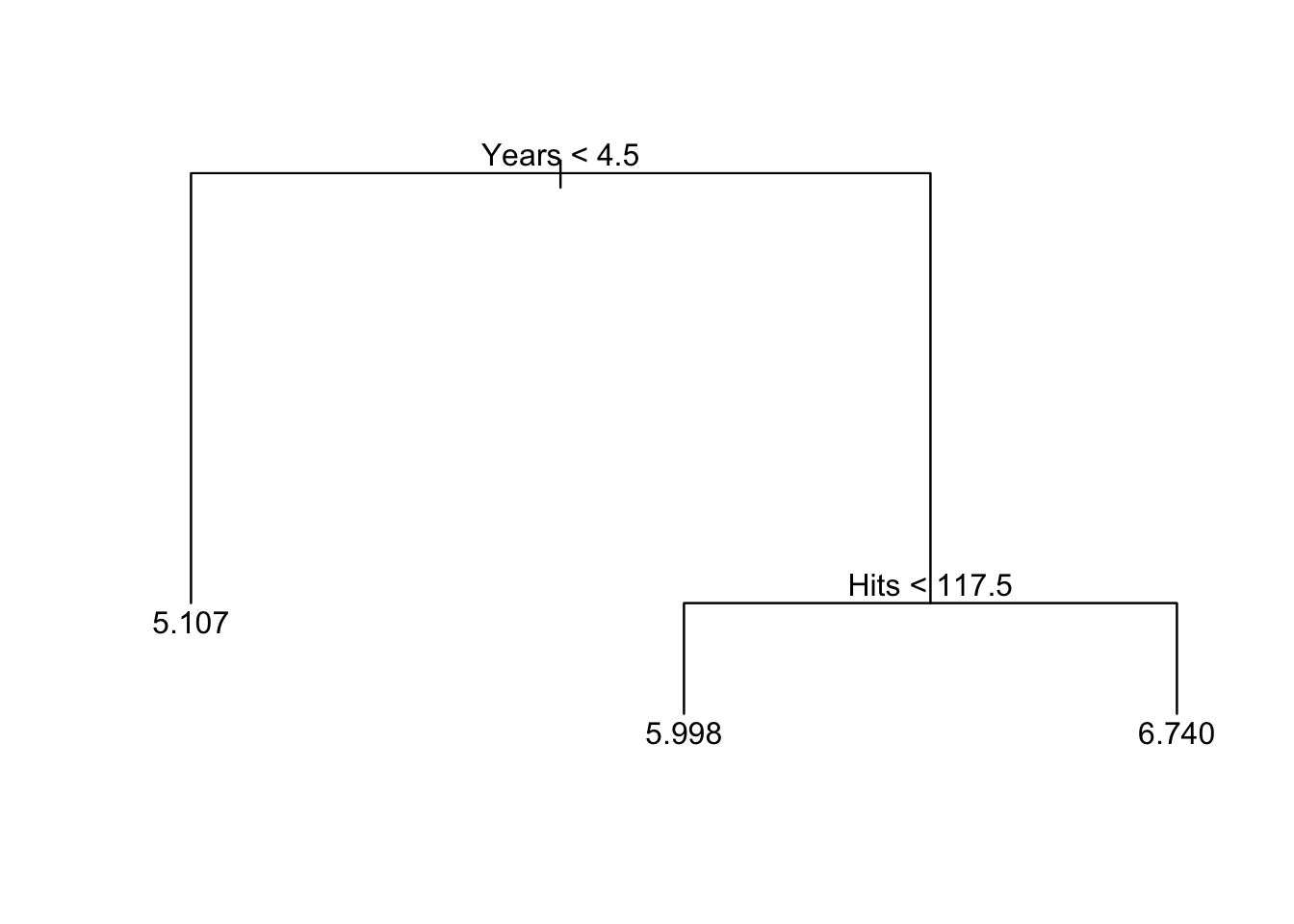

prune.hitters <- prune.tree(tree.hitters, best = 3)

summary(prune.hitters)##

## Regression tree:

## snip.tree(tree = tree.hitters, nodes = c(6L, 2L))

## Number of terminal nodes: 3

## Residual mean deviance: 0.3513 = 91.33 / 260

## Distribution of residuals:

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## -2.24000 -0.39580 -0.03162 0.00000 0.33380 2.55600plot(prune.hitters)

text(prune.hitters)

# if using the rpart package

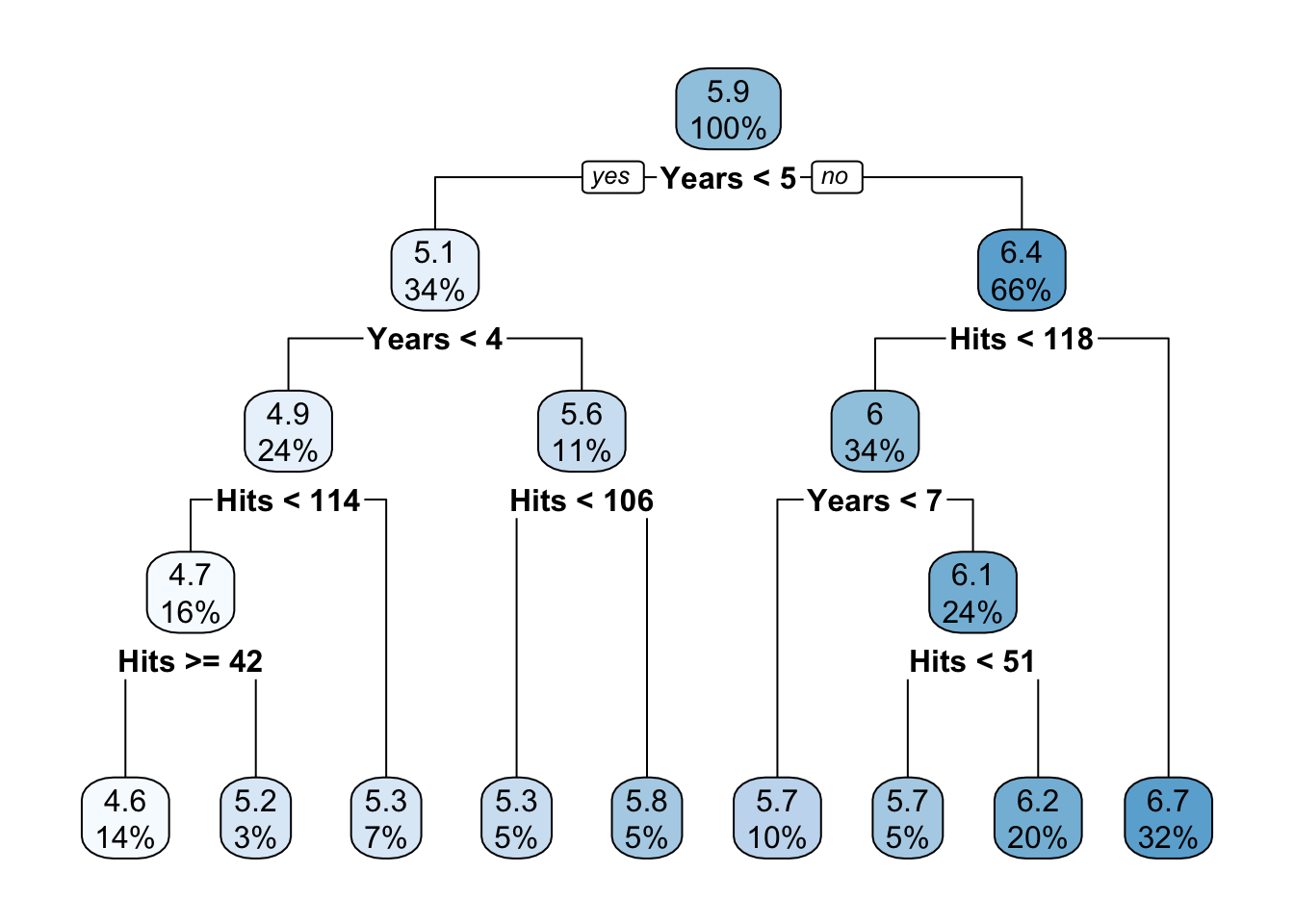

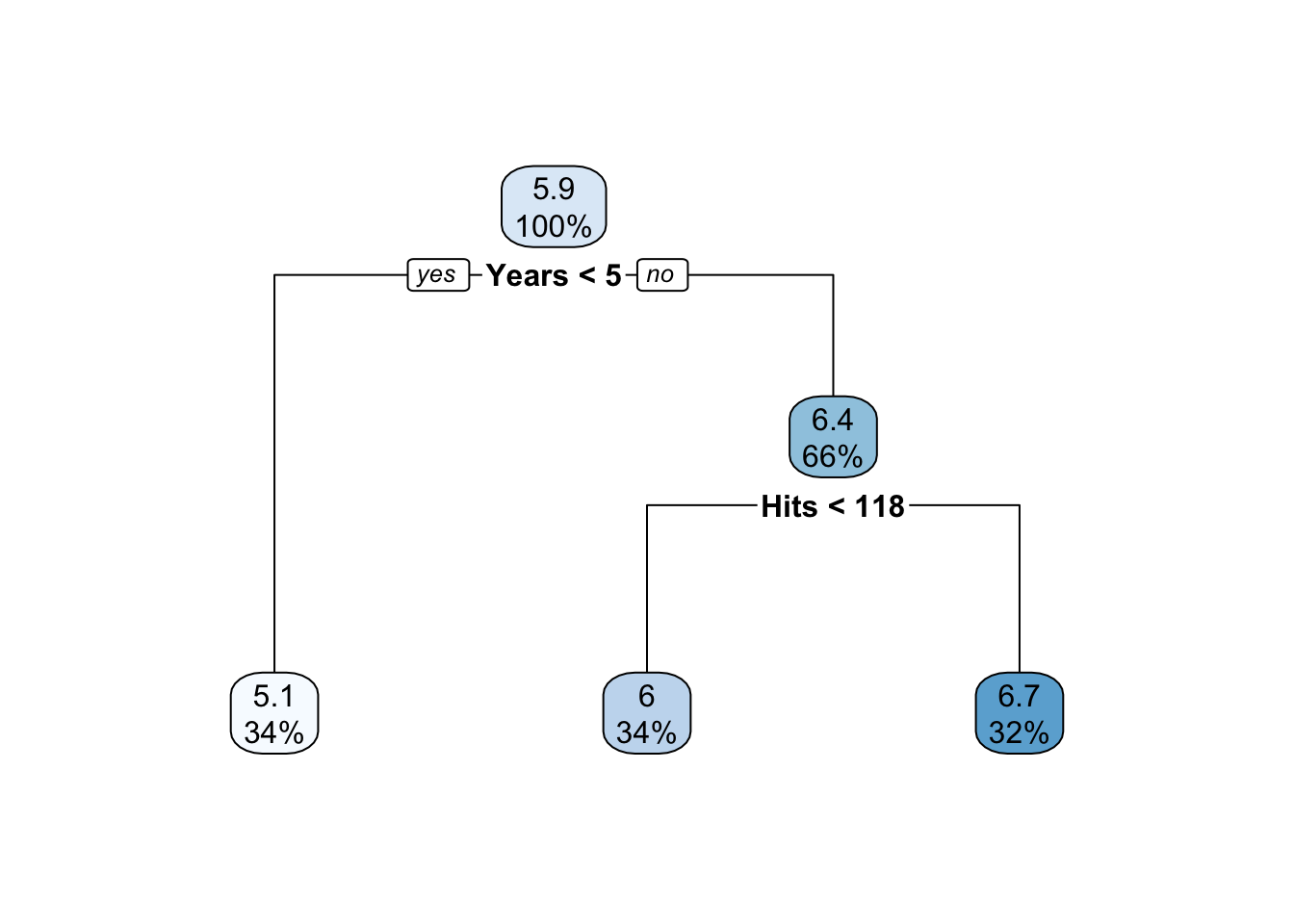

prune.hitters_2 <- rpart(formula = lgSalary ~.,

data = hitters[is.na(hitters$Salary) == F, c("lgSalary","Years","Hits")],

method = "anova",

control = list(cp = 0.1))

prune.hitters_2## n= 263

##

## node), split, n, deviance, yval

## * denotes terminal node

##

## 1) root 263 207.15370 5.927222

## 2) Years< 4.5 90 42.35317 5.106790 *

## 3) Years>=4.5 173 72.70531 6.354036

## 6) Hits< 117.5 90 28.09371 5.998380 *

## 7) Hits>=117.5 83 20.88307 6.739687 *rpart.plot(prune.hitters_2)

Cost Complexity Pruning

The cost complexity parameter is a tuning parameter for which we need to seek an optimal value through cross-validation.

hitters2 <- hitters[is.na(hitters$Salary)==F, c("lgSalary","Years","Hits","HmRun","RBI","PutOuts","Walks","Runs")]

set.seed(123)

train <- sample(1:nrow(hitters2), 132, replace=F)

# if using the tree package

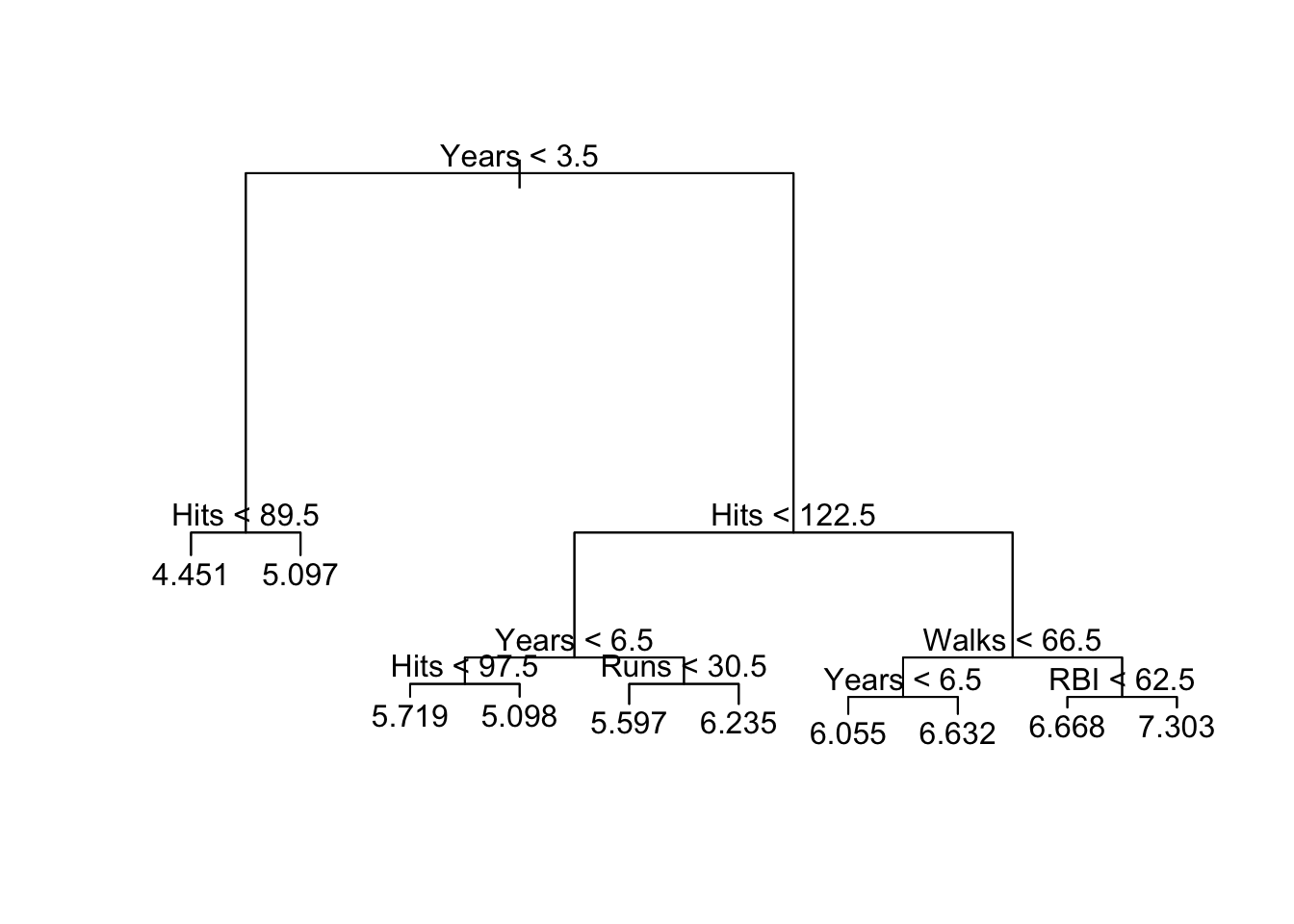

tree2.hitters <- tree(lgSalary~., hitters2[train,])

summary(tree2.hitters)##

## Regression tree:

## tree(formula = lgSalary ~ ., data = hitters2[train, ])

## Variables actually used in tree construction:

## [1] "Years" "Hits" "Runs" "Walks" "RBI"

## Number of terminal nodes: 10

## Residual mean deviance: 0.1857 = 22.65 / 122

## Distribution of residuals:

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## -1.555000 -0.202200 0.004768 0.000000 0.237100 1.156000plot(tree2.hitters)

text(tree2.hitters, pretty = 0)

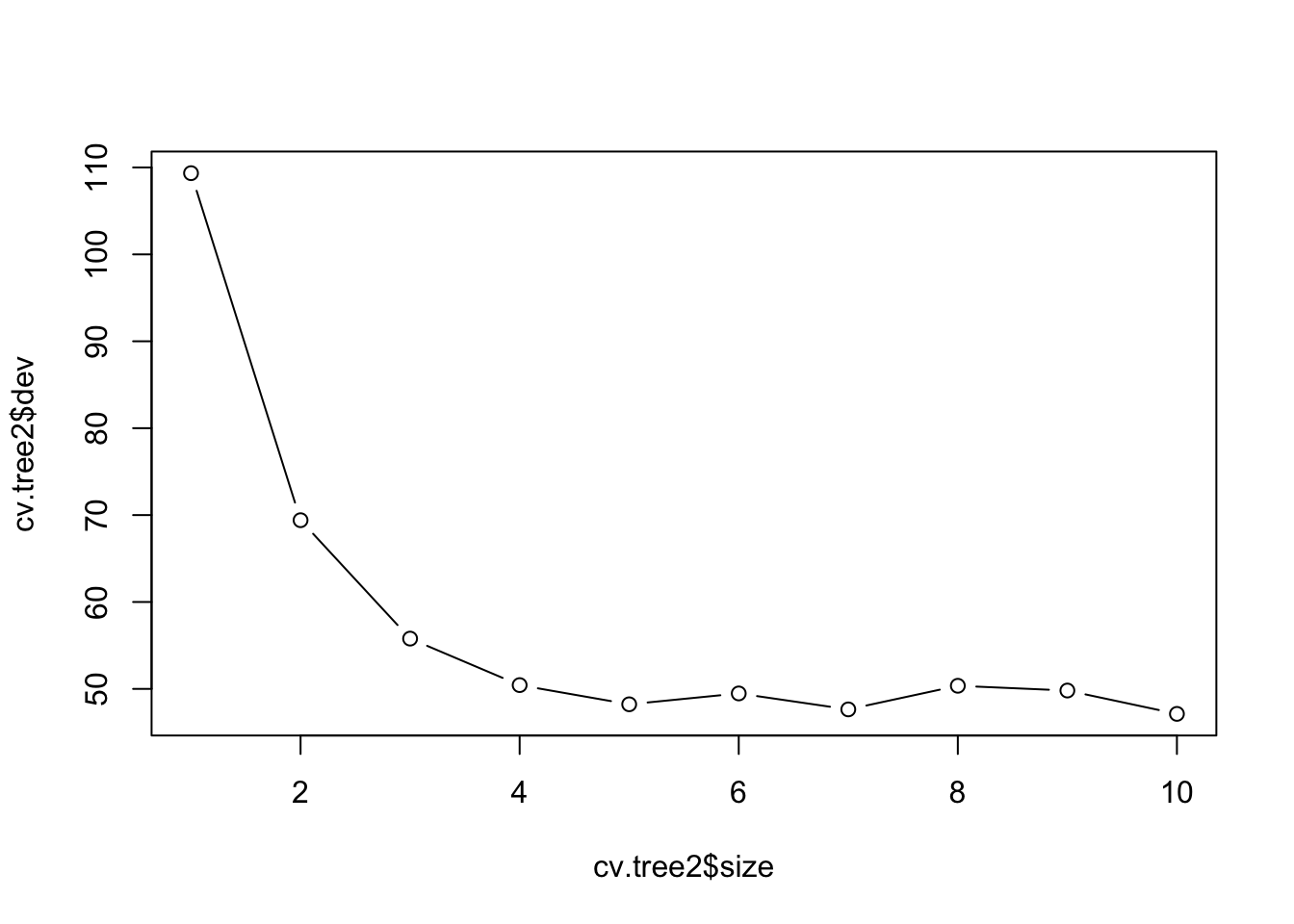

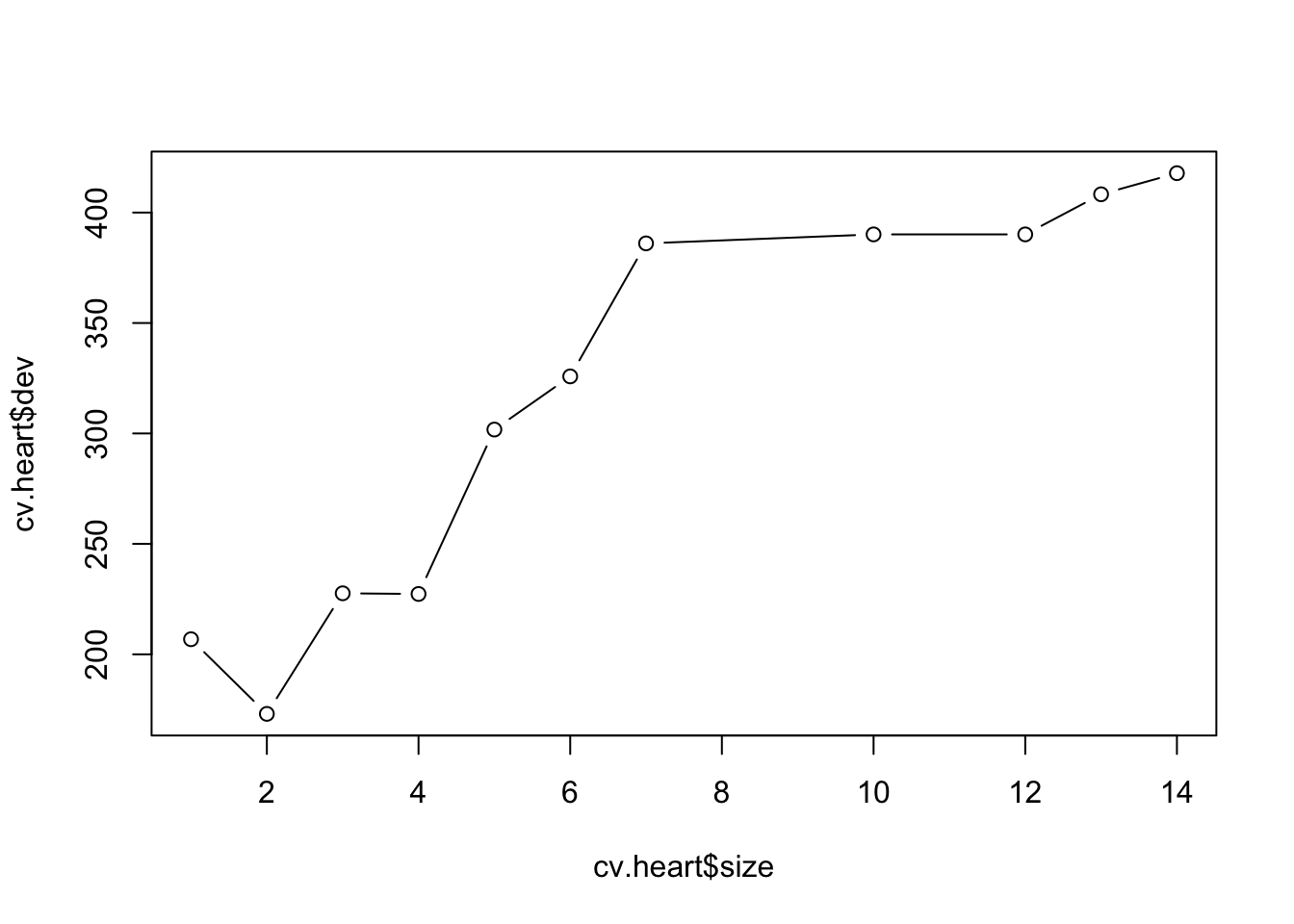

# pruning the tree via cross-validation

cv.tree2 <- cv.tree(tree2.hitters, K = 10)

plot(cv.tree2$size,cv.tree2$dev, type = "b")

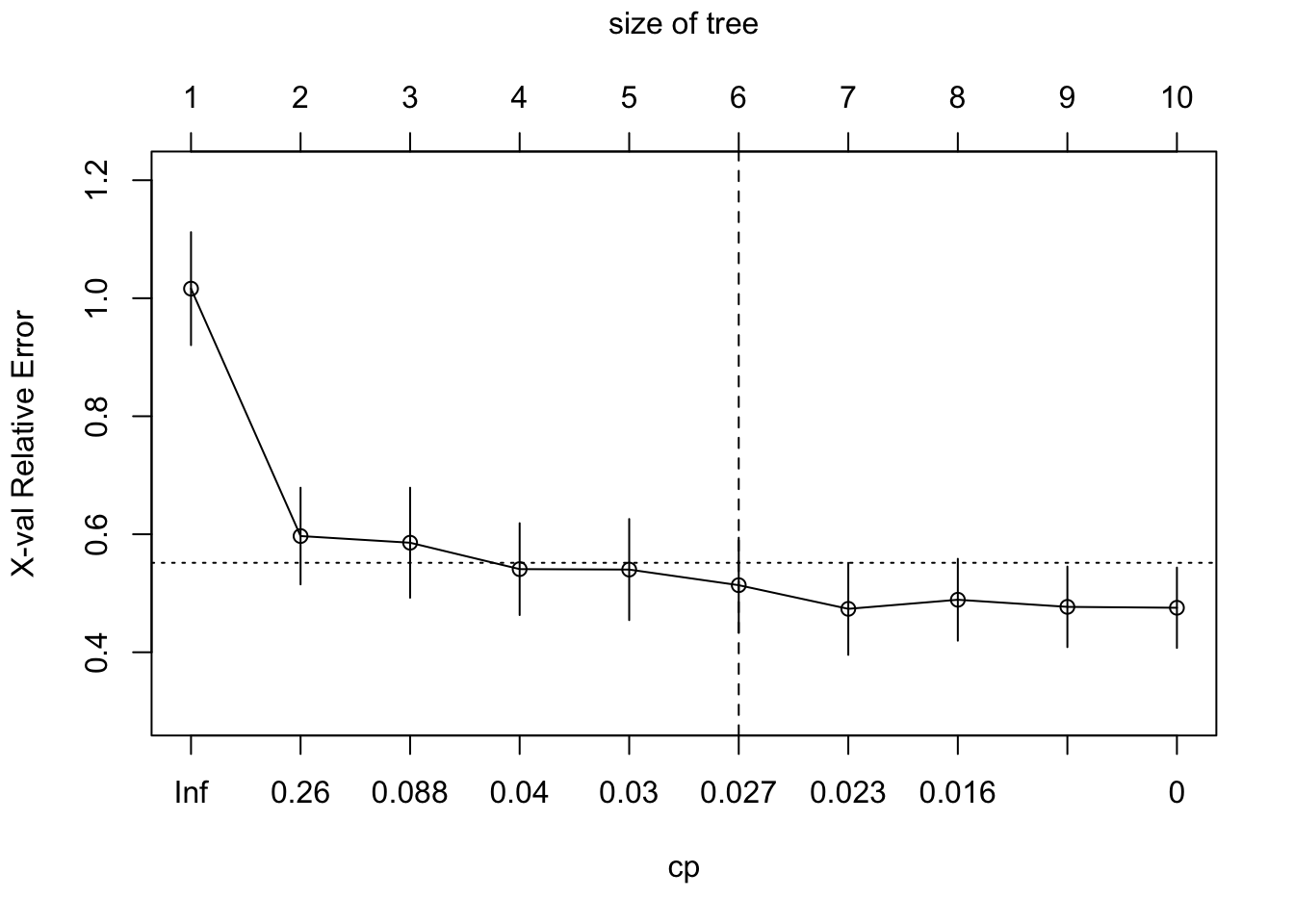

# if using the rpart package

tree2.hitters_2 <- rpart(formula = lgSalary ~.,

data = hitters2[train,],

method = "anova",

control = list(cp = 0, xval = 10)) #10-fold cv

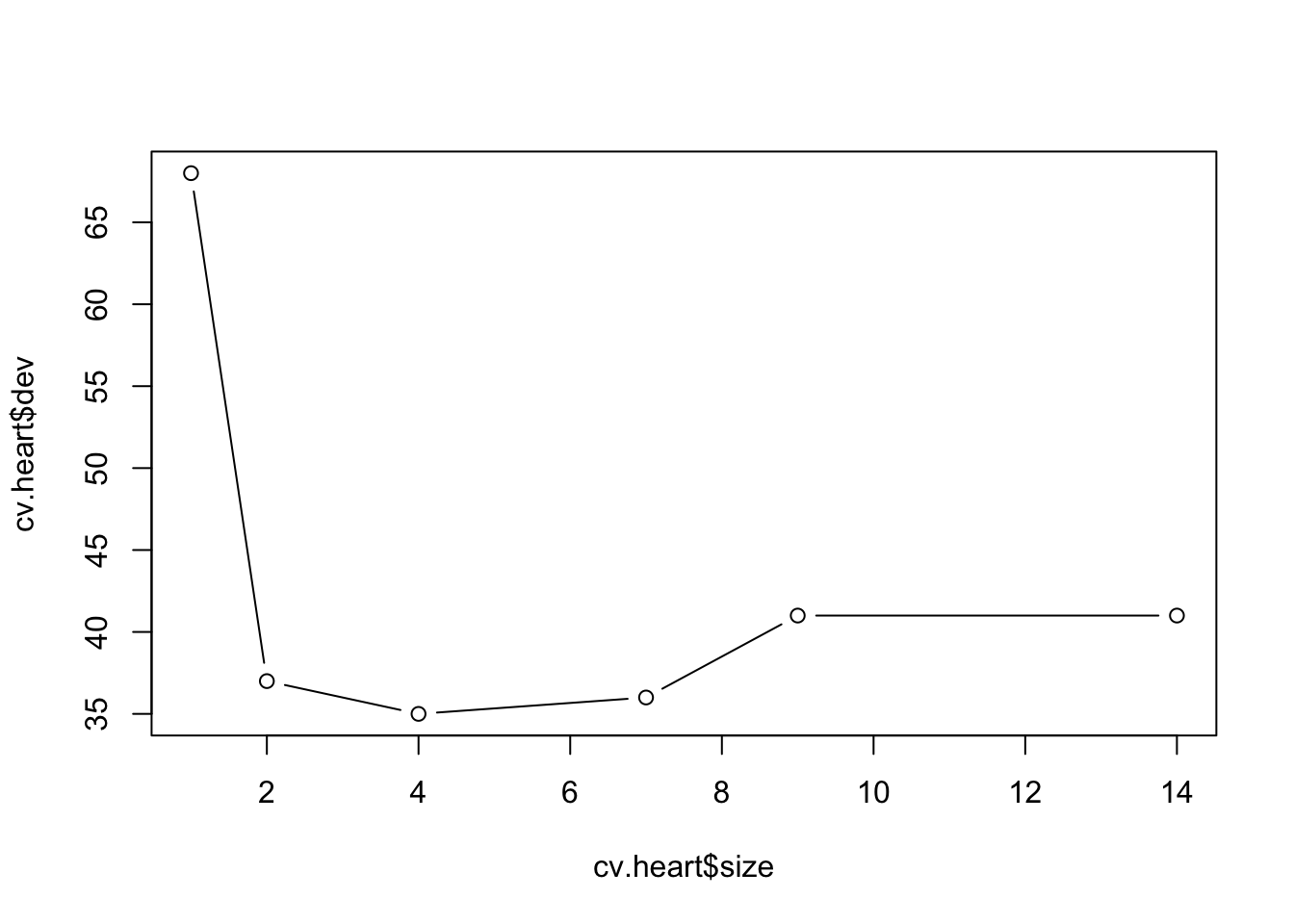

plotcp(tree2.hitters_2) # A good choice of cp for pruning is often the leftmost value for which the mean lies below the horizontal line.

abline(v = 6, lty = "dashed")

The cross-validation results suggest that we should keep four

terminal nodes using the tree package and 6 terminal nodes

using the rpart package.

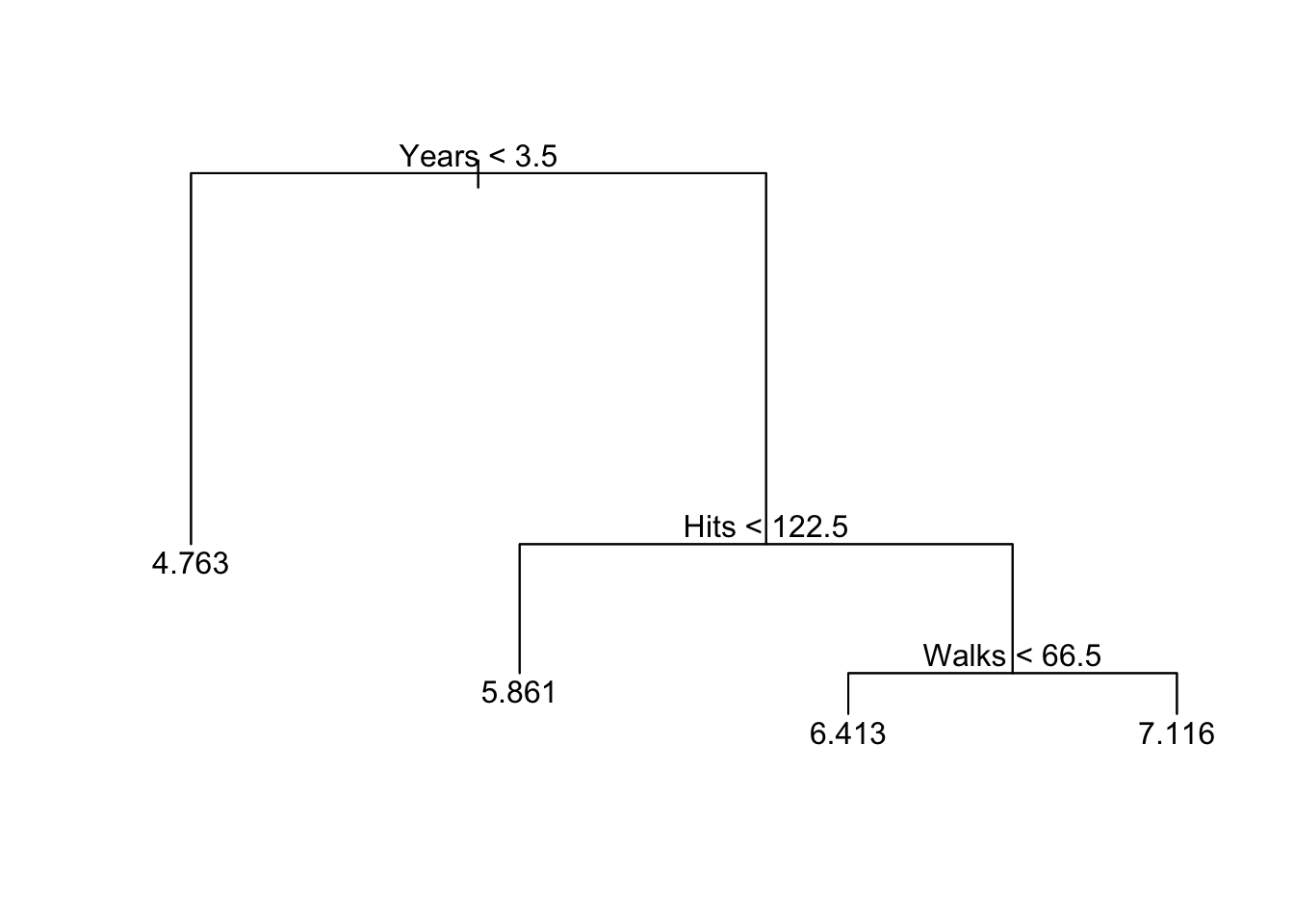

# if using the tree package

prune.hitters2 <- prune.tree(tree2.hitters, best = 4)

plot(prune.hitters2)

text(prune.hitters2)

# if using the rpart package

prune.hitters2_2 <- rpart(formula = lgSalary ~.,

data = hitters2[train,],

method = "anova",

control = list(cp = 0.027))

rpart.plot(prune.hitters2_2)

Classification Trees

In this example, we will use the patients’ data that contain a binary outcome HD for 303 patients who presented with chest pain. An outcome value of Yes indicates the presence of heart disease based on an angiographic test, while No means no heart disease. There are 13 predictors including Age, Sex, Chol (a cholesterol measurement), and other heart and lung function measurements such as Thal (Thallium stress test) and ChestPain symptoms.

We first fit a classification tree to the training data.

data("heart")

set.seed(1234)

train <- sample(1:nrow(heart), 150)

# if using the tree package

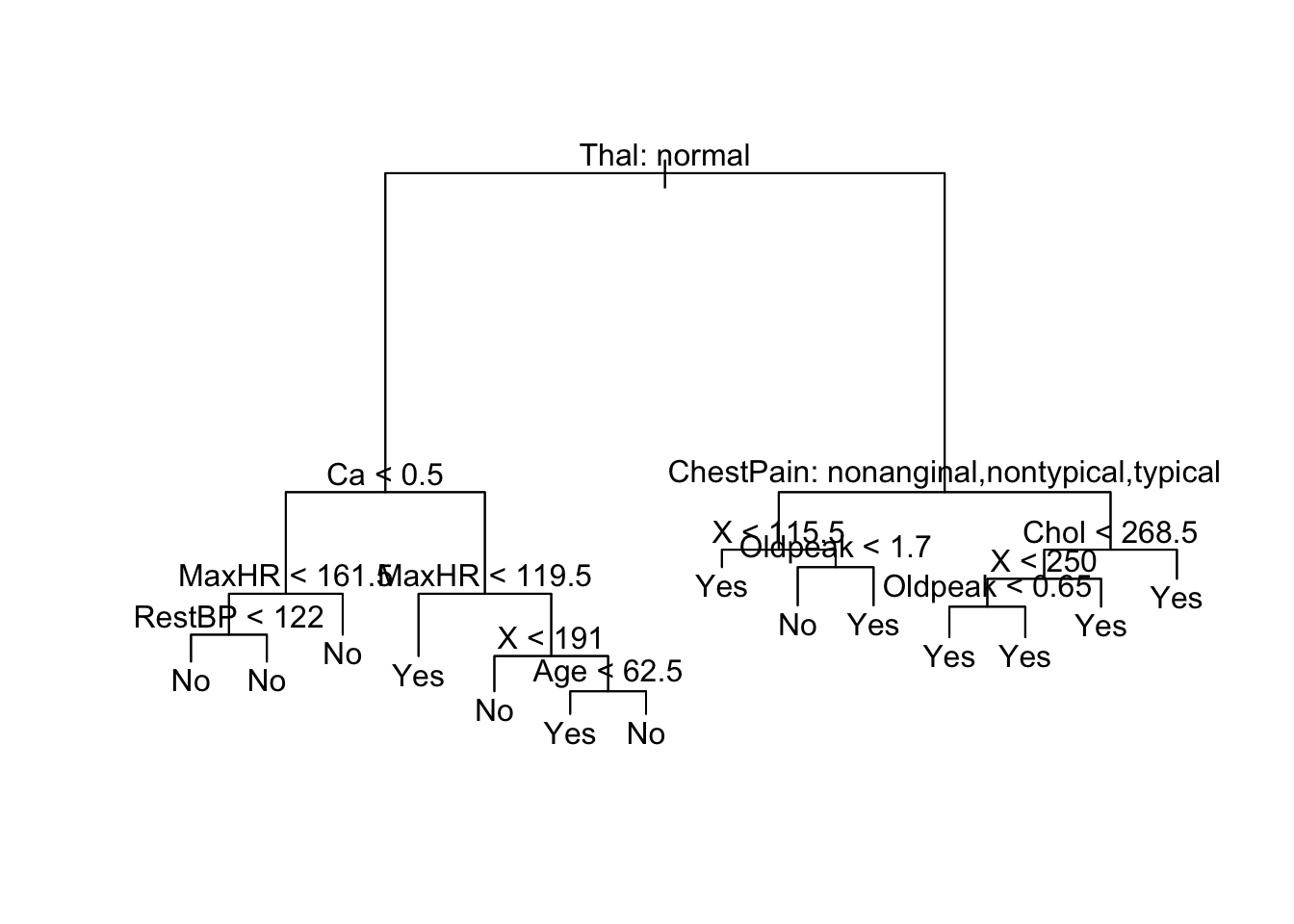

tree.heart <- tree(AHD ~ ., heart[train, ])

plot(tree.heart)

text(tree.heart, pretty = 0)

summary(tree.heart)##

## Classification tree:

## tree(formula = AHD ~ ., data = heart[train, ])

## Variables actually used in tree construction:

## [1] "Thal" "Ca" "MaxHR" "RestBP" "X"

## [6] "Age" "ChestPain" "Oldpeak" "Chol"

## Number of terminal nodes: 14

## Residual mean deviance: 0.4881 = 64.92 / 133

## Misclassification error rate: 0.102 = 15 / 147# if using the rpart package

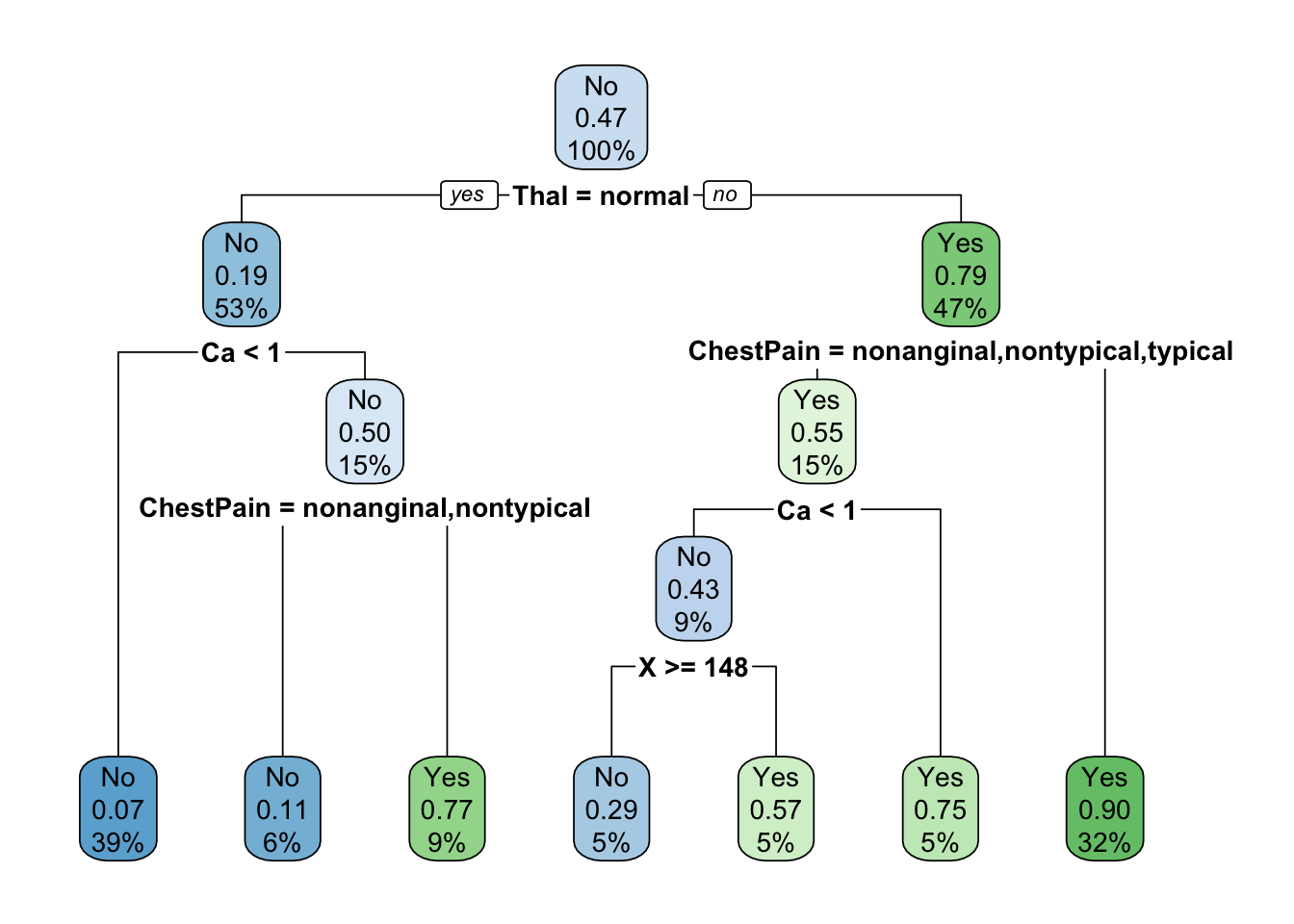

tree.heart_2 <- rpart(AHD ~ ., heart[train, ],

method = "class",

control = list(minsplit = 0, cp = 0, xval = 0))

tree.heart_2## n= 150

##

## node), split, n, loss, yval, (yprob)

## * denotes terminal node

##

## 1) root 150 70 No (0.53333333 0.46666667)

## 2) Thal=normal 80 15 No (0.81250000 0.18750000)

## 4) Ca< 0.5 58 4 No (0.93103448 0.06896552) *

## 5) Ca>=0.5 22 11 No (0.50000000 0.50000000)

## 10) ChestPain=nonanginal,nontypical 9 1 No (0.88888889 0.11111111) *

## 11) ChestPain=asymptomatic,typical 13 3 Yes (0.23076923 0.76923077) *

## 3) Thal=fixed,reversable 70 15 Yes (0.21428571 0.78571429)

## 6) ChestPain=nonanginal,nontypical,typical 22 10 Yes (0.45454545 0.54545455)

## 12) Ca< 0.5 14 6 No (0.57142857 0.42857143)

## 24) X>=148 7 2 No (0.71428571 0.28571429) *

## 25) X< 148 7 3 Yes (0.42857143 0.57142857) *

## 13) Ca>=0.5 8 2 Yes (0.25000000 0.75000000) *

## 7) ChestPain=asymptomatic 48 5 Yes (0.10416667 0.89583333) *rpart.plot(tree.heart_2)

Next we proceed to cross-validation to prune the classifications

tree.You could use different criterion for pruning by specifying the

method = argument when using the tree

package.

cv.heart <- cv.tree(tree.heart)

plot(cv.heart$size, cv.heart$dev, type = "b")

cv.heart <- cv.tree(tree.heart, method = "misclass")

plot(cv.heart$size,cv.heart$dev, type = "b")

prune.heart <- prune.tree(tree.heart, best = 2)

plot(prune.heart)

text(prune.heart,pretty=0)

# if using the rpart package

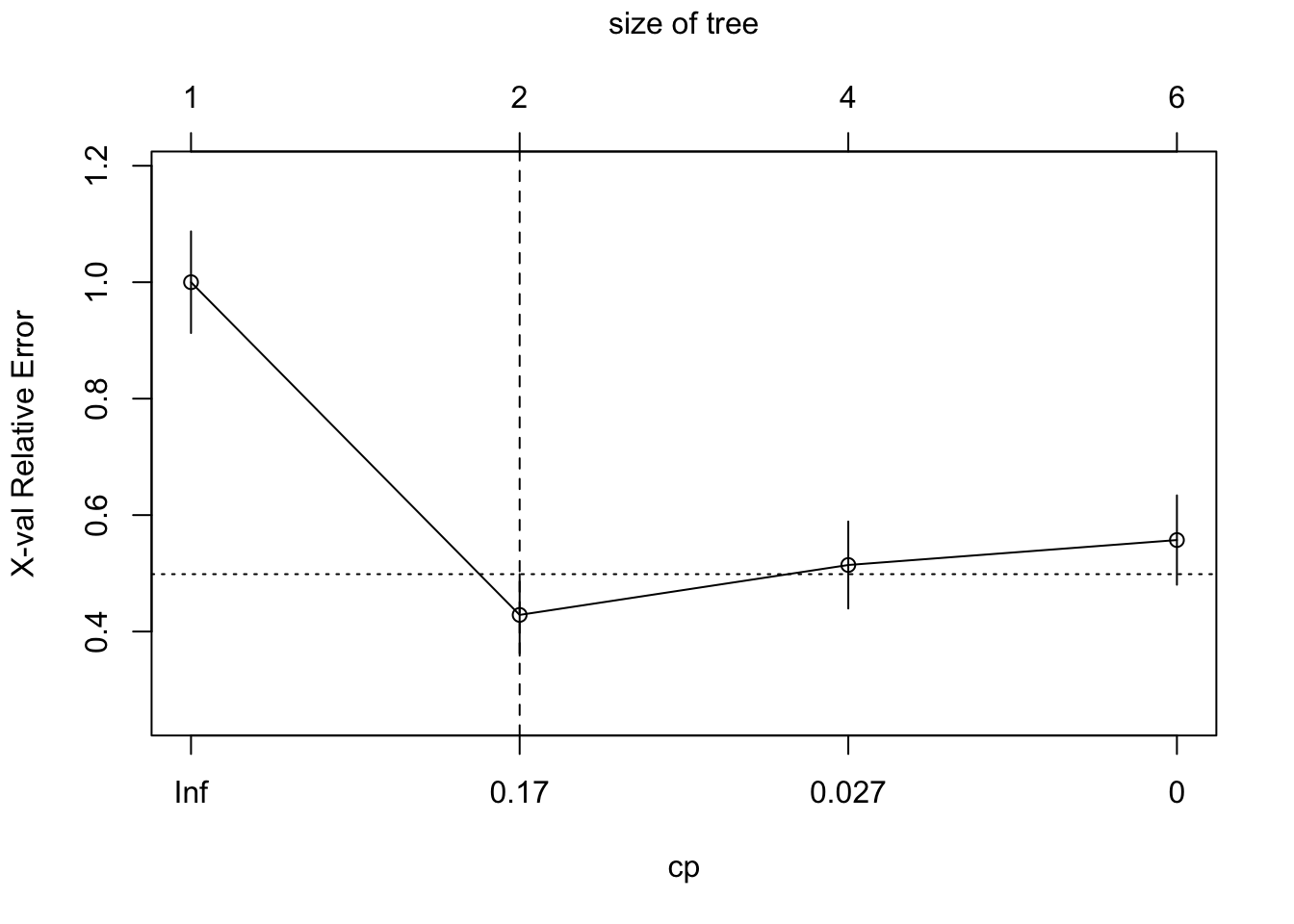

cv.heart_2 <- rpart(AHD ~ ., heart[train, ],

method = "class",

control = list(cp = 0, xval = 10))

plotcp(cv.heart_2)

abline(v = 2, lty = "dashed")

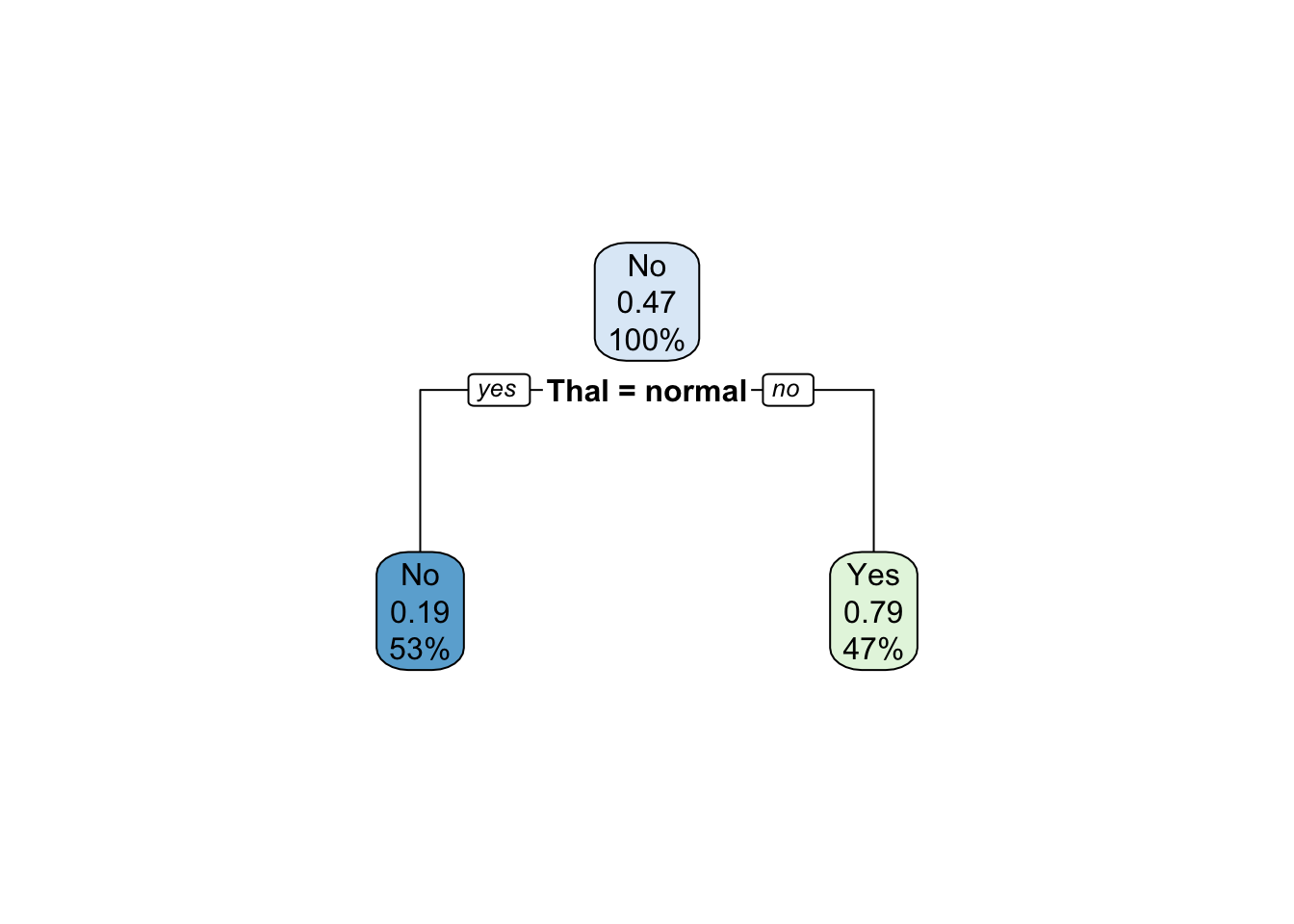

prune.heart_2 <- rpart(AHD ~ ., heart[train, ],

method = "class",

control = list(cp = 0.17))

rpart.plot(prune.heart_2)

Bagging

Bagging is a special case of random forest. Therefore, we could use

the randomForest package to implement bagging. But you have

to specify mtry= to be the total number of predictors in

the original data. Here we use the baseball data as an example.

set.seed(234)

train <- sample(1:nrow(hitters2), 132, replace=F)

(bg.hitters <- randomForest(lgSalary~., data=hitters2, subset=train, mtry=7, importance=T))##

## Call:

## randomForest(formula = lgSalary ~ ., data = hitters2, mtry = 7, importance = T, subset = train)

## Type of random forest: regression

## Number of trees: 500

## No. of variables tried at each split: 7

##

## Mean of squared residuals: 0.2571571

## % Var explained: 67.6Random Forest

We could implement random forest by changing the number of predictors

to be sampled at each split (mtry=). Here we use the

baseball data as an example.

(rf.hitters <- randomForest(lgSalary~., data=hitters2, subset=train, mtry=3, importance=T))##

## Call:

## randomForest(formula = lgSalary ~ ., data = hitters2, mtry = 3, importance = T, subset = train)

## Type of random forest: regression

## Number of trees: 500

## No. of variables tried at each split: 3

##

## Mean of squared residuals: 0.2407523

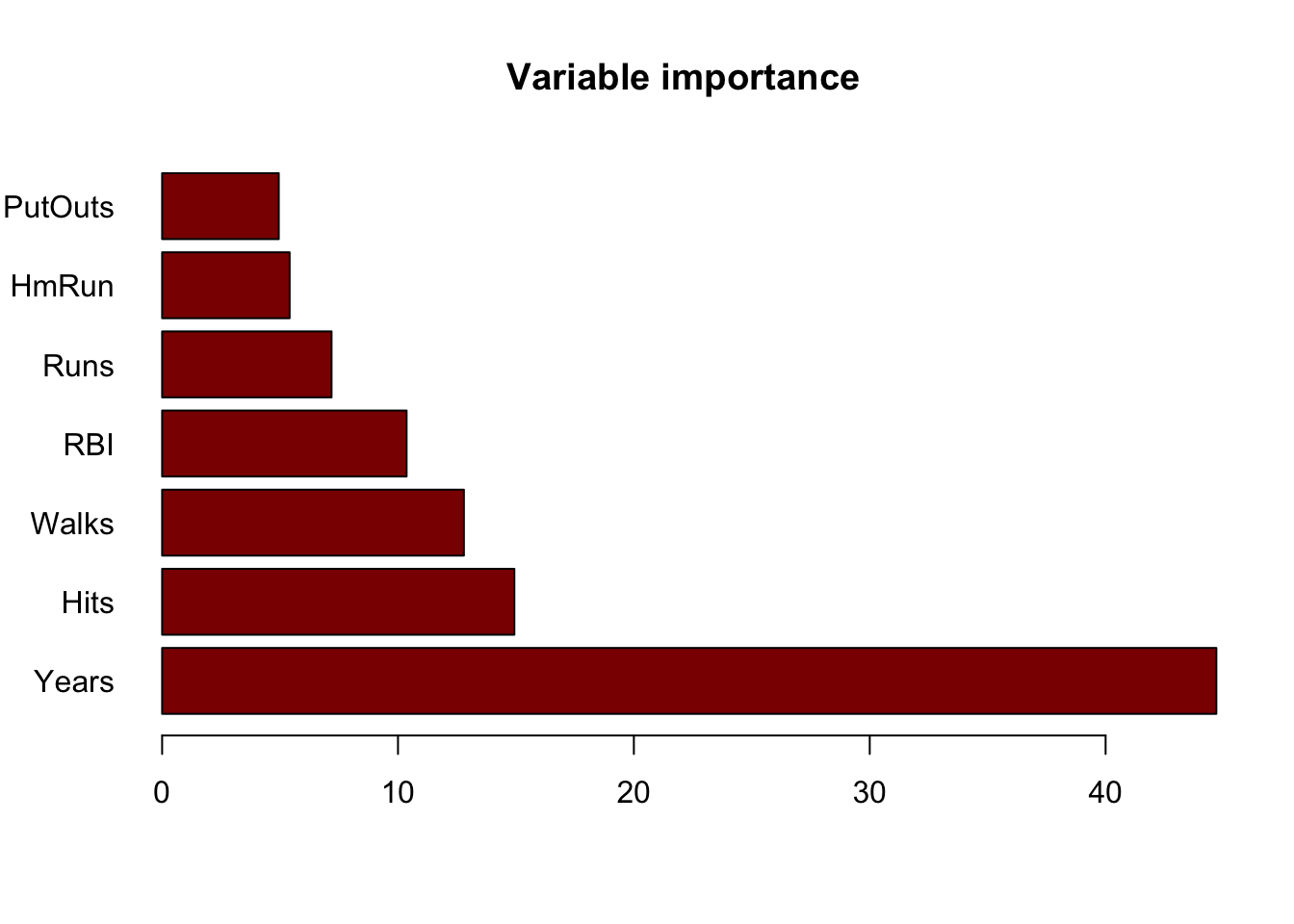

## % Var explained: 69.66Variable Importance Measures

imp.hitters <- importance(rf.hitters)

imp.hitters <- imp.hitters[order(imp.hitters[,2], decreasing=T),]

barplot(imp.hitters[,2], names.arg=rownames(imp.hitters), main="Variable importance", col="darkred", horiz=TRUE,las=1)

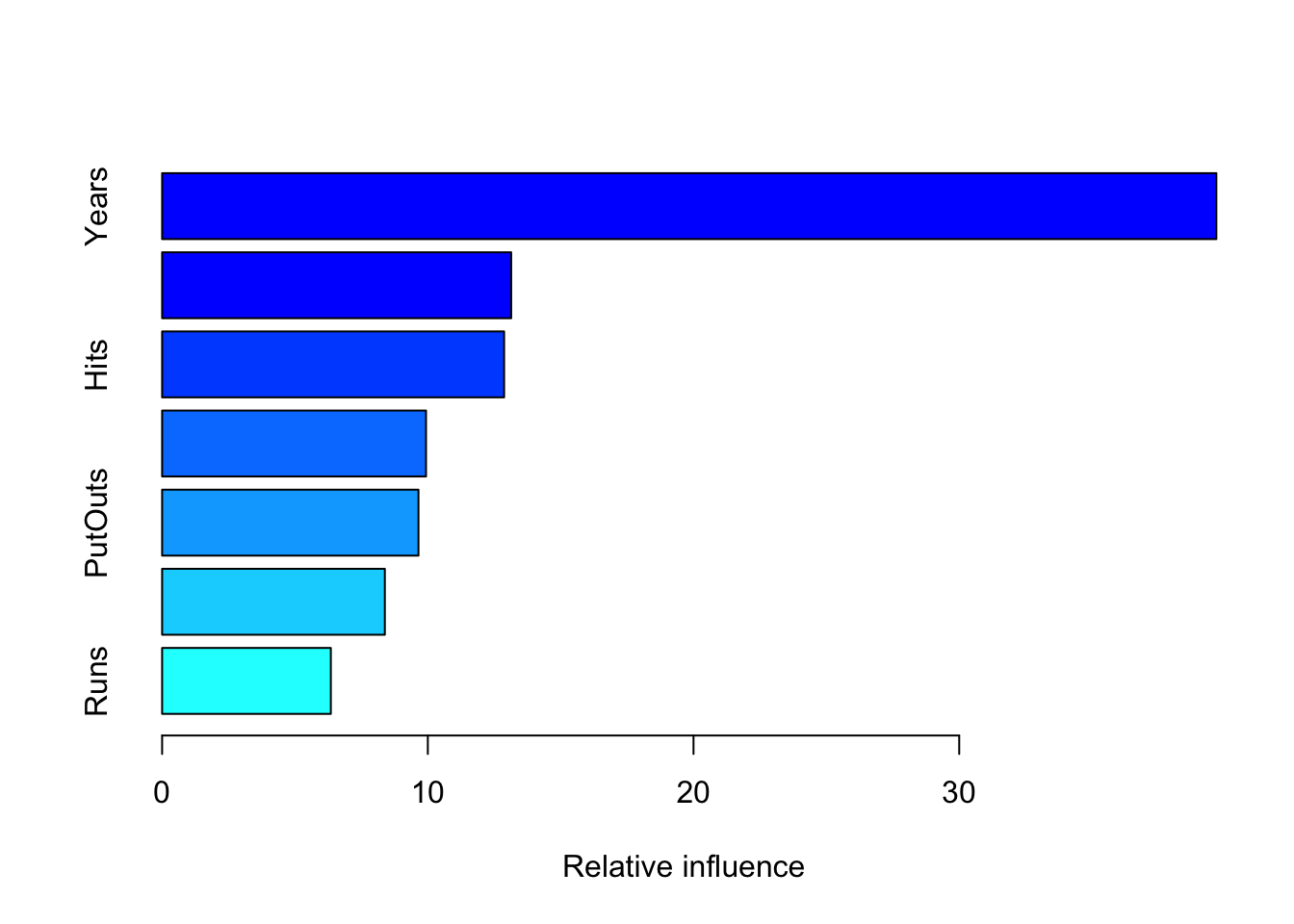

Boosting

We could use the gbm package to implement boosting. The

distribution = allows us to specify the loss function to be

used for gradient boosting. We use "gaussian" to tell R

that we would like to use the residual sum squared error in our

model.

set.seed(234)

train <- sample(1:nrow(hitters2), 132, replace=F)

boost.hitters <- gbm(lgSalary~., data=hitters2[train,], distribution="gaussian", n.trees = 10000, interaction.depth = 4, shrinkage=0.01, verbose=F)

summary(boost.hitters)

## var rel.inf

## Years Years 39.678225

## Walks Walks 13.137537

## Hits Hits 12.871641

## RBI RBI 9.932331

## PutOuts PutOuts 9.648024

## HmRun HmRun 8.382579

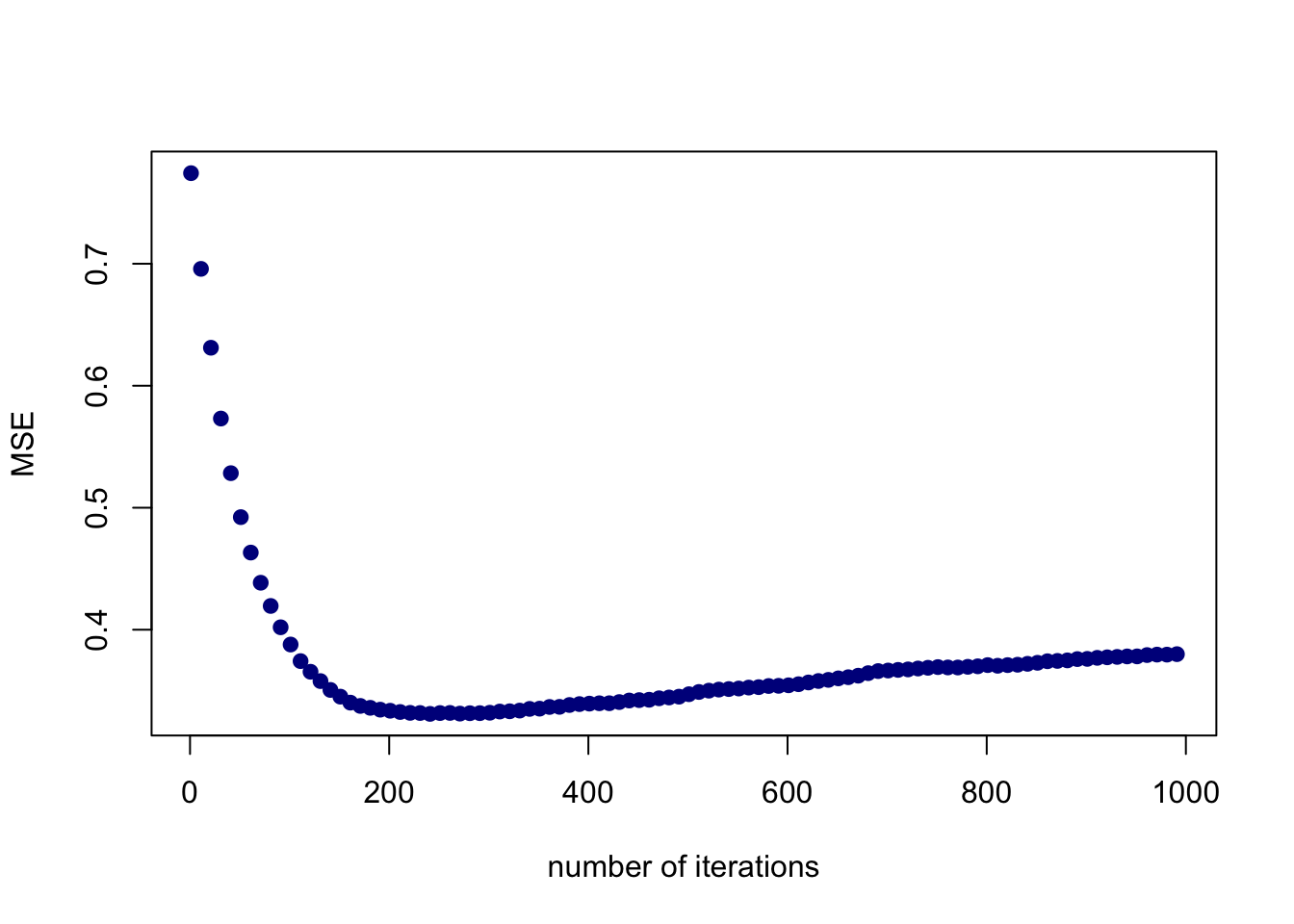

## Runs Runs 6.349663We could check how the validation error changes as the number of iterations increases.

ntrees <- seq(1,1000,10)

predmat <- predict(boost.hitters, newdata=hitters2[-train,], n.trees=ntrees)

boost.err <- apply((predmat-hitters2[-train, "lgSalary"])^2, 2, mean)

plot(ntrees, boost.err, pch=19, col="darkblue", ylab="MSE", xlab="number of iterations")

The R script for this tutorial can be found here.

This tutorial is adapted from the lab examples presented in the book “Introduction to Statistical Learning” authored by James, Witten, Hastie, & Tibshirani (2013).

© Copyright 2022 Yi Feng and Gregory R. Hancock.